Andrey Pirogov, founder of GISGeo Project, takes a look at mergers and acquisitions in the geospatial technology market from 2001 to September 2020.

Mergers and acquisitions, strategic partnerships and consortia are part of the usual business processes around the world. In some countries these processes are more noticeable, somewhere, as, for example, in Russia are less. The GISGeo project collected statistics of mergers and acquisitions in the geoinformation technology market from 2001 to September 2020.

Sources of information about transactions were news releases, company history records, databases (for example, Crunchbase). The databases we have analyzed, including commercial ones, do not always contain up-to-date and complete information.

We also cannot claim full coverage of all transactions. Information earlier than 2001 is difficult to find, so the research time frame is limited to the last 20 years.

We analyzed more than 500 transactions on the market and selected 208 for statistical analysis. The selected deals include only mergers and acquisitions of companies whose business profile is directly related to geoinformation technologies (remote sensing, geodesy, cartography, GIS development, navigation, geoanalytics, etc.). The analysis does not include transactions in which geographic information companies acquired suppliers or manufacturers of non-industry products (for example, financial services, steel smelting, etc.).

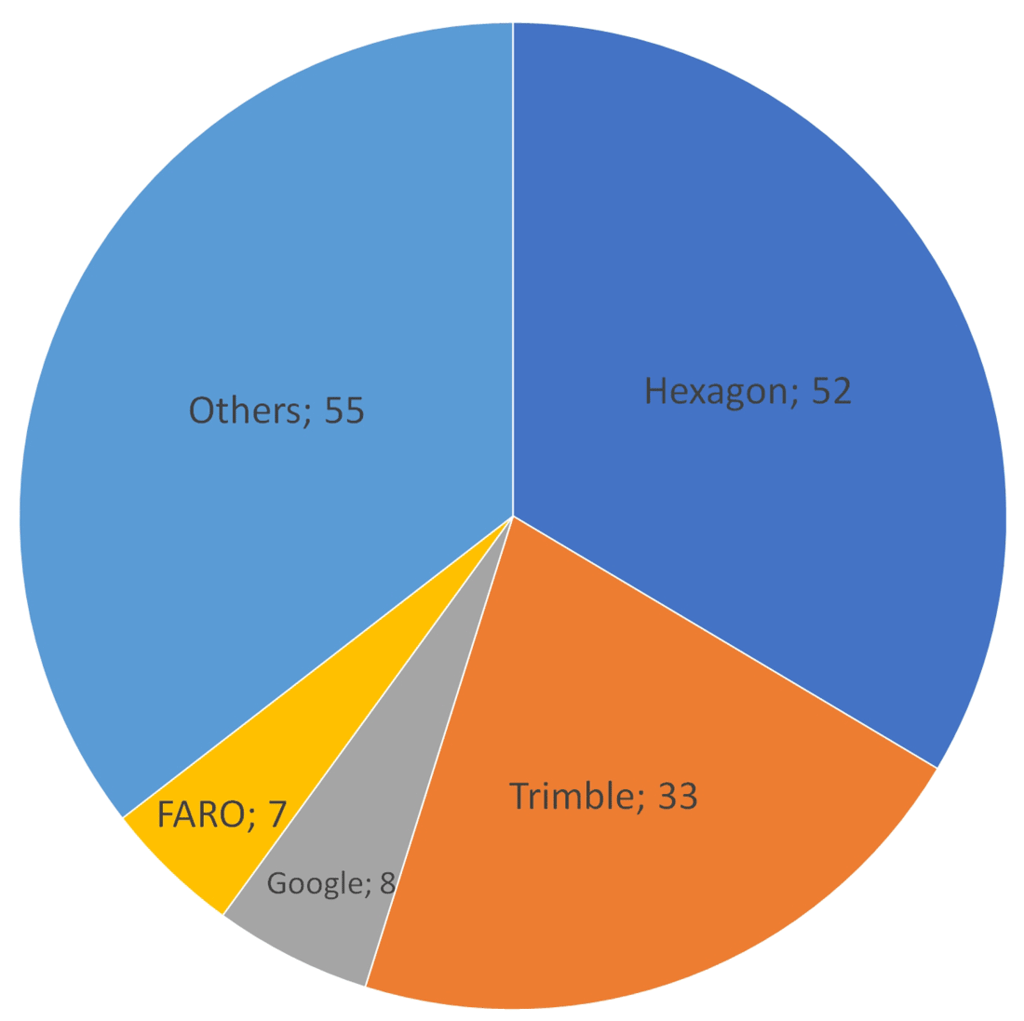

1. From 2001 to September 2020, 208 companies were acquired (acquired under certain conditions). The total number of buyers is 59 companies. Some of the buyers were later acquired by themselves.

See the full geospatial mergers and acquisitions table (pdf)

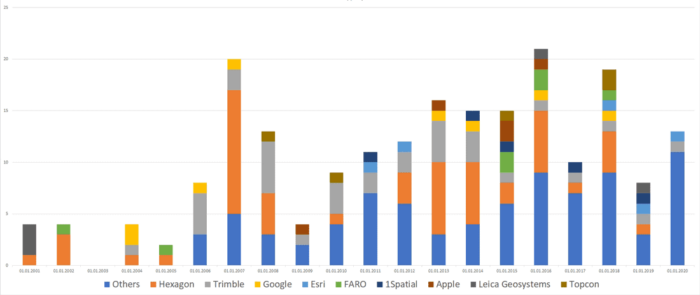

The total number of company transactions from 2001 to September 2020 is shown in the chart below.

As can be seen from the diagram, Hexagon (52) is the absolute leader in terms of the number of acquisitions, followed by Trimble (33), Google (8), FARO (7) and other companies follow with a significant lag.

2. The distribution by the number of purchases:

- 1 acquisition was made by 27 companies

- 2 acquisitions – 14 companies

- 3 acquisitions – 6 companies

- 4 acquisitions – 2 companies

- 5 acquisitions – 5 companies

- 7 acquisitions – 1 company

- 8 acquisitions – 1 company

- 33 acquisitions – 1 company

- 52 acquisitions – 1 company

3. More than half of all transactions in the market fell on 2 companies: Hexagon and Trimble.

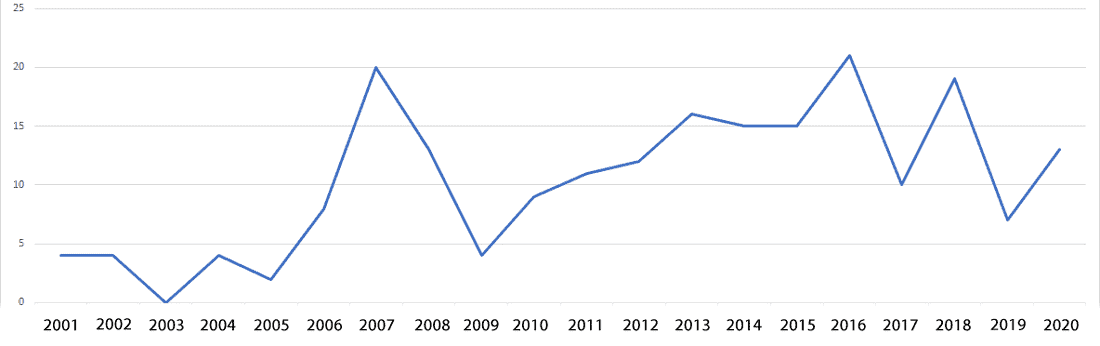

4. The dynamics of takeover processes (number of transactions per year) is shown in the graph below:

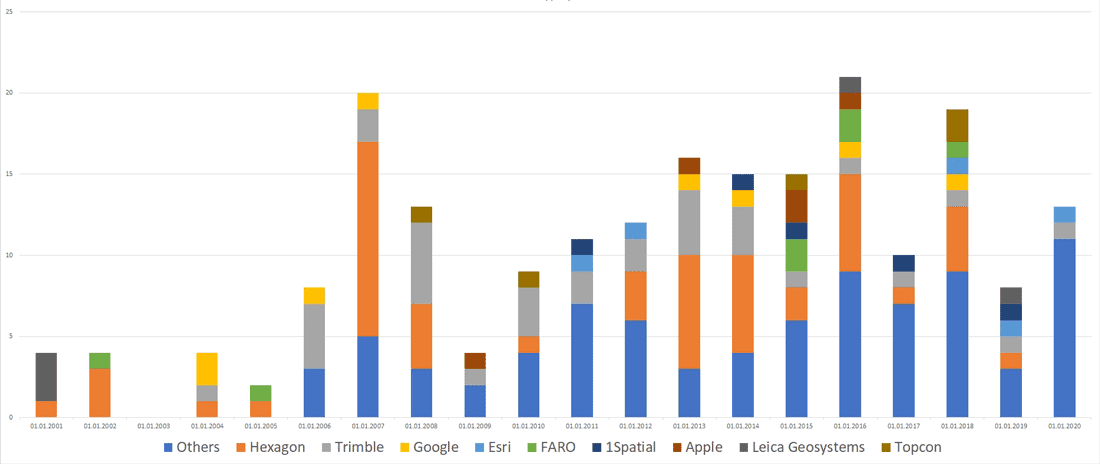

5. More interesting is the dynamics and the share of acquirer companies shown in the diagram below.

The processes of mergers and acquisitions in the market are quite active and it is obvious that they are not completed. The most ambitious player by far is Hexagon.

Most of the acquisitions can be called internal, they belong to the companies of the geoinformation market itself. There is no noticeable interest from representatives of retail, banking, consulting or finance in the geomatics industry.

It is noticeable that the number of players participating in the acquisition processes is increasing every year, and two key players, Hexagon and Trimble, have almost completed the active phase of acquisitions. Of course, our industry has an interesting future ahead.

About the Author

Andrey Pirogov is an expert in geospatial-related marketing management, GIS education, and geoscience-related research and project management. He is the head of marketing at Racurs, a Russia-based photogrammetric software company. Andrey Pirogov is a visiting lecturer at the Lomonosov Moscow State University Business School with an optional course “GeoInformation Technologies in Business”. He is a founder of GISGeo Project – the most active Russian-speaking community in the field of geomarketing and GIS-analytic.